Category Archives: Oil services

HUNT-NO (BUY, TP NOK 3.3): Initiation of New VLCC Pure-Play

Mr. Arne Fredly is in the process of re-branding failed Oslo-listed oil service company Hunter Group (former Badger Explorer) into a VLCC pure-play, infusing four VLCC newbuilds plus three optional berths at DSME. Given our view of ~70% asset price appreciation...

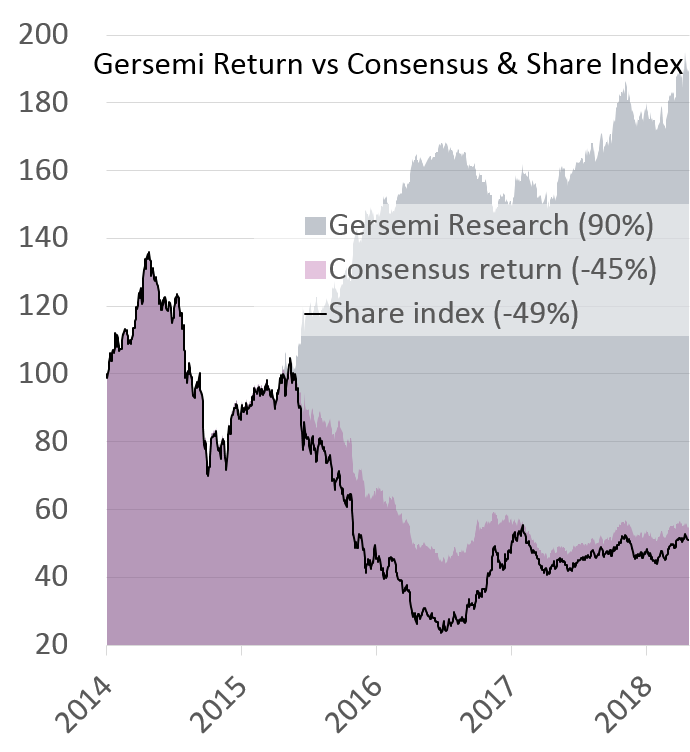

2018: Firing on all Cylinders (26-page report)

Never before have we been so optimistic across all sub-segments of the shipping/oil service sectors simultaneously as we now are for 2018. All segments have either just entered the expansionary phase of the business cycle, or will experience the inflection...

Posted in _Public, dry bulk, LNG carriers, LPG shipping, Oil services, oil tankers, rig, shipping, VLGC

Tagged 2020-no, ALNG-NO, avance-no, BDRILL-NO, bulk-no, BWLPG-NO, DHT-US, dsx-us, egle-us, ESV-US, EURN-US, FLNG-NO, FRO-US, GLOG-US, gnk-us, gogl-us, LPG-US, NAT-US, NE-US, NODL-NO, RDC US, salt-us, sb-us, sblk-us, sbulk-no, ship-us, SOFF-NO, tnk-us

2 Comments

SOFF-NO (BUY, TP 10) Initiation

We initiate coverage of Solstad Farstad with a BUY recommendation and target price of NOK 10. We estimate a NAV/sh of NOK 12.6, but this estimate is extremely elastic to movements in fleet values due to an estimated adjusted equity...

NE-US: Initiation (BUY, TP 12)

We initiate coverage of Noble Corporation with a BUY recommendation and target price of USD 12

The company has a large fleet of attractive assets, a balanced contract backlog and a decent liquidity position. We believe the company is well positioned to take advantage of the looming expansionary phase of the cycle.

RDC-US: Initiation (BUY, TP 20)

We initiate coverage of Rowan Companies with a BUY recommendation and target price of USD 20

The company has a fleet of four UDWs and 25 jackups of which only two are currently stacked. The company's earnings visibility is strong based on the current contract backlog, further supported by the recently announced JV with Saudi Aramco. Add to this a coffer of USD 1.3bn and improving earnings ahead, we deem the company a defensive investment at the trough, but with the a free option on a cyclical recovery.

ATW-US: Initiation (BUY, TP 19)

We initiate coverage of Atwood Oceanics with a BUY recommendation and target price of USD 19

The company has four modern UDWs/Drillships and five modern Jackups on the water, in addition to an aging Deepwater rig and two UDW newbuildings stacked at DSME until 2019/20 but deliverable at Atwood's option.

ESV-US: Initiation (BUY, TP 17)

We initiate coverage of Ensco with a BUY recommendation and target price of USD 17

The company has 59 rigs on the water in addition to two deferred newbuildings, a market cap of USD 2.5bn and is on of the most liquid names in the industry. Despite this, we estimate the company is trading at a discount to NAV and an implied 3% discount per rig at current trough levels.

NODL-NS: Initiation (BUY, TP 90)

We initiate coverage of Northern Drilling with a BUY recommendation and target price of NOK 90

All the time Seadrill remains in disarray, Northern Drilling has emerged as the new investment vehicle for Fredriksen ahead of the next cyclical upturn in the rig space. The company currently has two more or less complete semi-sub newbuildings warehoused at HHI, and the main assumption is for delivery in Jan/19.

BORR-NS: Update (BUY, TP 60[54])

Borr Drilling today announced the LOI to purchase Transocean’s 15 jackups in addition to a USD 800m equity offering. The accretive nature of these corporate events leads us to raise our target price to NOK 60 (from 54). As we highlighted...

SONG-NO: Initiation (BUY, TP 47)

We initiate coverage of Songa Offshore with a BUY recommendation and target price of NOK 47 Songa Offshore has an EV/M.cap of 6.2 (implied 16% equity ratio) and has four modern rigs on long-term contracts to Statoil until 2022/24 (three vintage...

BORR-NS: Initiation (BUY, TP 54)

We initiate coverage of Borr Drilling with a BUY recommendation and target price of NOK 54 The company is still in its cocoon, and we believe it is about to become a butterfly at an opportune time in the cycle. Recent chatter links...