Tag Archives: shipping

Tanker consolidation continues with TNK acquiring TIL

Teekay Tankers today announced the acquisition of Tanker Investments in an all-share deal which values TIL at a 21% premium to last close and which reflects a NAV-for-NAV transaction on our estimates. TIL’s shareholder will end up with 38% of...

Posted in oil tankers

Tagged shipping, tanker investments, Teekay Tankers, til, til-no, TNK, tnk-us

Leave a comment

GNRT-US: Initiation (SELL, TP 3.8)

Gener8 Maritime emerged in 2015 as the result of the merger between General Maritime and Navig8 Crude Tankers. The company has a fleet of 38 oil tankers trading spot, consisting of 23 VLCCs, 10 Suezmaxes and five Aframaxes/Panamaxes. GNRT is highly leveraged and...

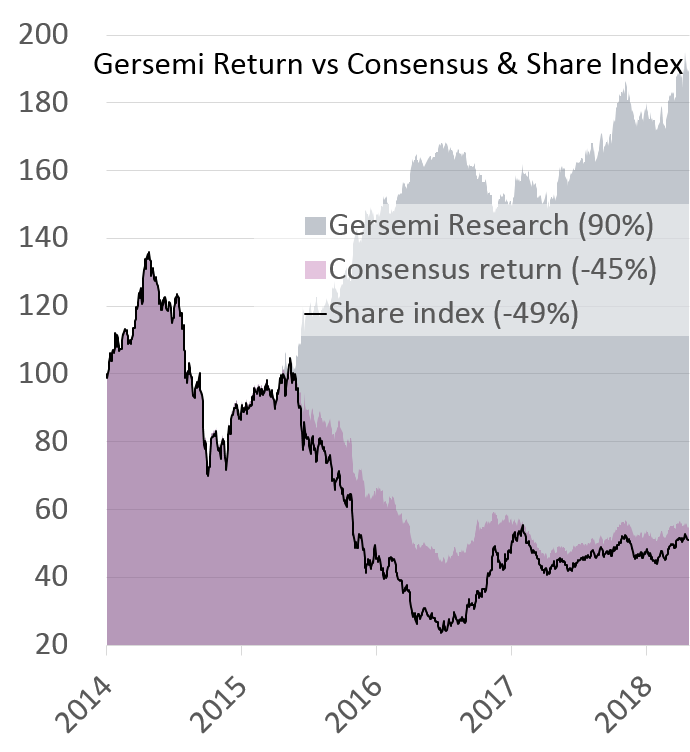

TIL-NO: Initiation (SELL, TP 33)

Originally set up as a well-timed asset play in early 2014, the company managed to divest a small portion of its fleet before the cycle turned to recession in 2016. Thus, the focus has shifted to operations ahead of the...

GLOG-US: Initiation (BUY, TP 18)

We initiate coverage of GasLog with a BUY recommendation and target price of USD 18. The company has a fleet of 27 LNG Carriers (including five newbuldings) with a contract coverage of 76% in 2017 and an average minimum back-log per contracted vessel of ~5.5 years. Although the secured cash-flow enables the company to pay dividends even at the trough (current annualized dividend yield at 8%), it also equates to less operational leverage at what we believe to be the expansionary point in the cycle from mid-'17. In addition, GasLog is exploring possibilities within the booming FSRU segment, and has an attractive source of financing trough its MLP (at least in the current environment of low interest rates). We find low risk and great valuation in GasLog and initiate coverage with a BUY recommendation and TP of USD 18.

Posted in Uncategorized

Tagged GasLog, GLOG, GLOP, LNG, LNG carriers, LNG tankers, shipping

7 Comments

Dry Bulk Appendix

As a response to popular demand, we have compiled a couple of asset specific slides as an appendix to our Dry Bulk: Sector Update from 4 April 2017. Disclaimer: The publisher currently owns shares in EGLE-US...

FLNG-NO: Initiation (BUY, TP 17)

We initiate coverage of Flex LNG with a BUY recommendation and target price of NOK 17.

The company has no vessels on the water in the current trough, but four MEGI LNGC newbuildings scheduled for delivery in 2018. Given our view that the trough is finally coming to an end in 2q17 and that the expansionary phase of the cycle is imminent, we find the setup of Flex extremely attractive. Adding the strong sponsor in Mr Fredriksen, we see additional upside from future accretive deals and positive bias from investment banker analysts.

Posted in Uncategorized

Tagged Flex LNG, FLNG, FLNGF, LNG, LNG carriers, LNG tankers, shipping

6 Comments

SHIP-US: Initiation (BUY, TP 1.25)

We initiate coverage of Seanergy Maritime with a BUY recommendation and target price of USD 1.25.

The company has made some very attractive acquisitions at the bottom of the cycle, one example being the two 2010-built Korean Capes which have appreciated ~60% since the deal was announced six months ago.

We see recent equity issuances as accretive given the appreciation of asset prices. However, we believe a discount on the company vs peers is just given several factors; including the At-The-Market (ATM) program, recent fee structure, the class A Warrants and share illiquidity.

Valuation: Our target price of USD 1.25/sh is based on a NAV of USD 0.94/sh, but added value from the optionality of a further 10% increase in asset values which would equate to a NAV of 1.67/sh, and applying a 25% discount. The implied asset value elasticity of NAV is 79% in our calculations, which is attractive given our view of rising asset prices, but equally sensitive on the downside... We recommend the less risk averse investor to BUY the share.

Dry Bulk: Sector Update

The first quarter of the year definitely surprised on the upside in terms of seasonally high earnings and rising asset prices. The latter is natural when considering that most listed players have a strong currency in its share price after the recent surge, and we have seen several very accretive shares-for-ships type deals. Although we have a positive view on the dry bulk sector, we are lukewarm to the shares as too much of the cyclical upturn is already priced in. Earnings are lagging with a median EV/EBITDA of 28x in 2017E and 17x in 2018E on our estimates. Thus, we find the current valuation too steep, although with a few company-specific deviations. Any potential fall in share prices could represent an excellent opportunity to buy.