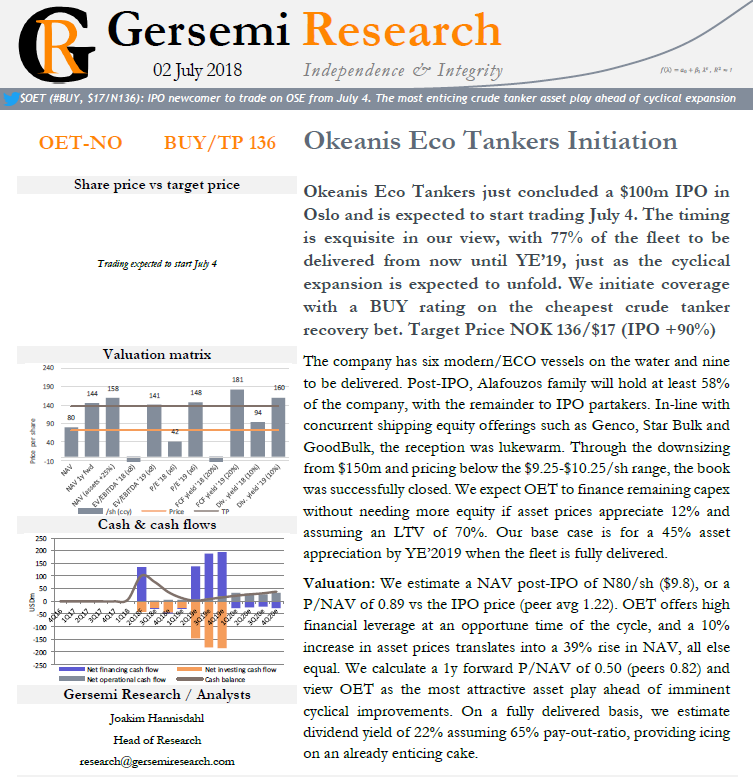

Okeanis Eco Tankers just concluded a $100m IPO in Oslo and is expected to start trading July 4. The timing is exquisite in our view, with 77% of the fleet to be delivered from now until YE’19, just as the cyclical expansion is expected to unfold. We initiate coverage with a BUY rating on the cheapest crude tanker recovery bet. Target Price NOK 136/$17 (IPO +90%)

The company has six modern/ECO vessels on the water and nine to be delivered. Post-IPO, Alafouzos family will hold at least 58% of the company, with the remainder to IPO partakers. In-line with concurrent shipping equity offerings such as Genco, Star Bulk and GoodBulk, the reception was lukewarm. Through the downsizing from $150m and pricing below the $9.25-$10.25/sh range, the book was successfully closed. We expect OET to finance remaining capex without needing more equity if asset prices appreciate 12% and assuming an LTV of 70%. Our base case is for a 45% asset appreciation by YE’2019 when the fleet is fully delivered.

Valuation: We estimate a NAV post-IPO of N80/sh ($9.8), or a P/NAV of 0.89 vs the IPO price (peer avg 1.22). OET offers high financial leverage at an opportune time of the cycle, and a 10% increase in asset prices translates into a 39% rise in NAV, all else equal. We calculate a 1y forward P/NAV of 0.50 (peers 0.82) and view OET as the most attractive asset play ahead of imminent cyclical improvements. On a fully delivered basis, we estimate dividend yield of 22% assuming 65% pay-out-ratio, providing icing on an already enticing cake.

Please download the full report for supporting graphs and tables

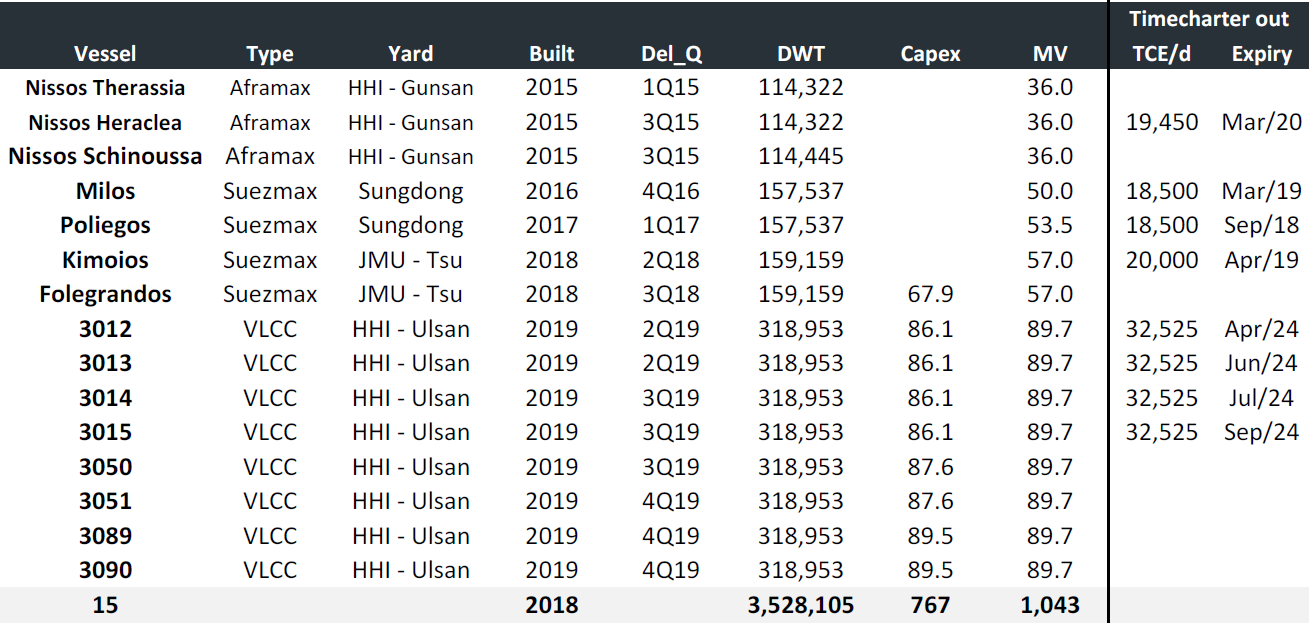

Fleet overview

Okeanis has one of the most modern fleets among listed crude tankers, with all vessels built from January 2015 or later. All VLCC newbuildings will be scrubber fitted and IMO’20 compliant, with retrofitting planned for all three Aframaxes and four Suezmaxes in 2019/20. The entire fleet have Ballast Water Treatment Systems in place.

One of the few negative attributes of OET is that four out of the eight VLCC newbuildings are chartered out on long charters at $32,525/d, reducing operational leverage. The charters are on strong rates comparative to the $19k/d VLCC spot average over the past two years, but 37% below our average $52k/d forecast for the charter periods.