As we have argued time and again since our initiation in May 2017, Teekay Tankers would need to abolish dividends, seek a debt moratorium and/or do more sale/leasebacks in order to survive the trough without a dilutive equity issuance. In the 1Q18 report today, the company finally announced the abolishment of dividends in addition to a further seven sale/leasebacks. Although it might have come as a surprise to some investors as the share price fell around 6% on the news to reach almost all-time-low levels, we view it as positive news as it mitigates our longstanding liquidity concerns.

We now forecast a positive cash position for TNK throughout our forecast period until 2021, for the first time. Although still a concern, we reduce our company-specific discount from 20% to 10%, and lift our target price from $1.2 to $1.3. In concert with the falling share price, it leads us to upgrade TNK from a HOLD to a BUY.

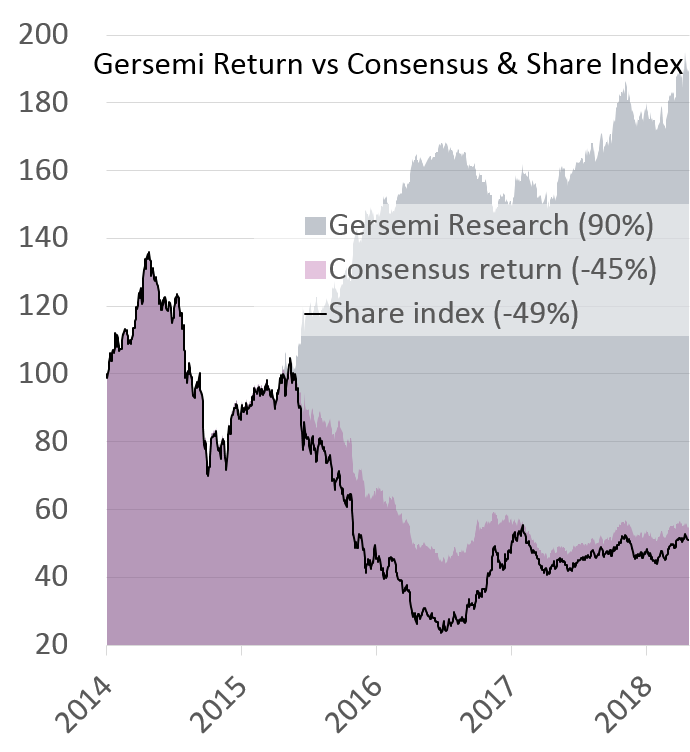

Since our initiation, we have a 44% return on our recommendations while consensus has 0% and the share price is -47%

We bought TNK at $1.11 today. Godspeed to us all…