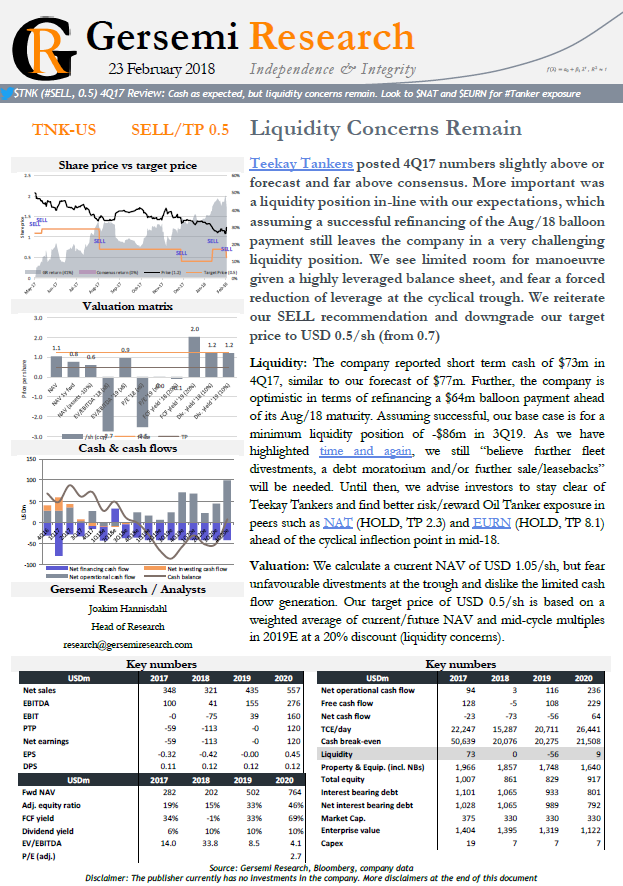

Teekay Tankers posted 4Q17 numbers slightly above or forecast and far above consensus. More important was a liquidity position in-line with our expectations, which assuming a successful refinancing of the Aug/18 balloon payment still leaves the company in a very challenging liquidity position. We see limited room for manoeuvre given a highly leveraged balance sheet, and fear a forced reduction of leverage at the cyclical trough. We reiterate our SELL recommendation and downgrade our target price to USD 0.5/sh (from 0.7)

Liquidity: The company reported short term cash of $73m in 4Q17, similar to our forecast of $77m. Further, the company is optimistic in terms of refinancing a $64m balloon payment ahead of its Aug/18 maturity. Assuming successful, our base case is for a minimum liquidity position of -$86m in 3Q19. As we have highlighted time and again, we still “believe further fleet divestments, a debt moratorium and/or further sale/leasebacks” will be needed. Until then, we advise investors to stay clear of Teekay Tankers and find better risk/reward Oil Tanker exposure in peers such as NAT (HOLD, TP 2.3) and EURN (HOLD, TP 8.1) ahead of the cyclical inflection point in mid-18.

Valuation: We calculate a current NAV of USD 1.05/sh, but fear unfavourable divestments at the trough and dislike the limited cash flow generation. Our target price of USD 0.5/sh is based on a weighted average of current/future NAV and mid-cycle multiples in 2019E at a 20% discount (liquidity concerns).